- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

Sui Q1 Advanced Report: The Rise of BTCfi Infrastructure, the Boom of Lending Protocols, and the Future of Rollup-Based Scalability

Original Title: Sui's Q1 Wrapped: BitcoinFi, MEV, and Scaling

Original Author: Delphi Digital

Original Translation: Glendon, Techub News

Since Delphi Digital's last in-depth exploration of Sui's architecture, ecosystem, and tokenomics, the network has completed a series of key upgrades in its infrastructure and application stack. In this follow-up report, we will analyze the ecosystem's key developments, including the build-out of Bitcoin Finance (BTCfi) infrastructure, the growth trajectory of the lending protocol Suilend, and the expansion of Aftermath Finance's footprint.

In terms of infrastructure, the launch of Mysticeti v2 introduced a "Fast Path" for low-fee transactions, significantly reducing latency and rebalancing validator workloads. Meanwhile, Move VM 2.0 achieved significant execution improvements through advanced composability, region-based memory management, modular architecture, and enhanced features designed to support more complex and dynamic on-chain logic.

Simultaneously, Sui's scaling roadmap has continued to evolve with the advancement of Pilotfish execution sharding to achieve true horizontal scalability and flexible validator configurations. These improvements in Sui were further reinforced by implementing localized object-based fee markets and MEV-aware optimizations (including priority transaction inclusion and consensus block ordering).

Ecosystem Updates

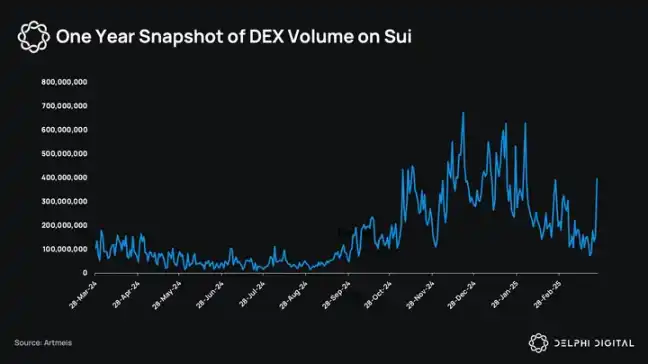

DEX trading volume on Sui has decreased from the previous quarter's peak, but it can be observed that following the launch of the WAL token of the decentralized storage protocol Walrus on March 27, trading volume has seen an increase.

BTCfi on Sui

BTCfi has recently emerged as a niche market on Sui, bringing lending, staking, and yield basics to Bitcoin, traditionally seen as passive collateral. According to DeFiLlama, the total value locked (TVL) in the BTCfi space has grown from less than $100 million to over $4.5 billion, covering various assets such as re-collateralization, anchoring, and decentralized BTC.

By the end of 2024, Sui announced a partnership with Babylon Labs and Lombard Protocol to introduce native BTC staking through LBTC. LBTC is a liquidity staking token minted directly by Lombard on the Sui and Cubist platforms, aimed at assisting users with deposit, minting, cross-chain, and staking management. Several weeks later, in December 2024, Sailayer collaborated with LBTC and WBTC to launch a BTC re-staking opportunity for LBTC and WBTC. Prior to this, the Lorenzo Protocol had introduced stBTC on Sui, a Babylon-driven liquidity staking token designed to aggregate BTC yields and integrate with DeFi protocols like Cetus and Navi. In early February 2025, Sui Bridge added support for wrapped BTC assets such as WBTC and LBTC, with over 587 BTC flowing into the Sui DeFi platform since then.

So far, over $111 million worth of wrapped BTC has been deposited into Sui-native protocols such as Suilend, Navi, and Cetus.

DeFi Protocols on Sui

Suilend

Suilend is a lending protocol in the Sui ecosystem, and within less than a year of operation, its annualized revenue reached $15 million in February 2024, with 70% flowing into the SEND treasury. The treasury initially received 1.2 million SUI from the "mdrop."

Suilend also introduced an Automated Market Maker (AMM) called Steamm, featuring an integrated money market component designed to maximize capital efficiency by depositing idle liquidity into the lending market. The protocol has a composable architecture supporting various pricing systems, including constant product pricing, stablecoin-centric pricing, and market volatility-based dynamic fee pricing. By allowing idle funds to earn yield in the lending market while remaining available for trading, Steamm enhances capital efficiency and provides additional returns to liquidity providers through its bToken mechanism.

Aftermath

MetaStables, incubated by Aftermath on Sui, serves as a treasury system that allows users to deposit cross-chain or native assets to mint stablecoins such as mUSD (pegged to the US dollar) and mETH (pegged to ETH), with plans to introduce meta-tokens like mBTC in the future. It facilitates slippage-free trading between treasury assets based on oracle-provided exchange rates (e.g., Pyth), avoiding the inefficiencies of AMM slippage and supporting lending of deposited assets to boost returns. MetaStables aims to address liquidity fragmentation by promoting meta-tokens and enabling users to earn mPOINTS.

In addition to MetaStables, Aftermath has also launched Perp DEX on the testnet, which is a fully Sui-native on-chain perpetual contract order book.

Walrus Goes Live

The decentralized storage protocol Walrus launched its mainnet on March 27, 2025, and completed a $140 million funding round led by Standardcrypto.

Walrus is a decentralized storage network built on Sui designed to store various types of data, from NFT assets and AI model weights to blockchain archives and website content. It can also serve as a data availability layer for rollups, similar to Celestia or EigenDA. While Walrus leverages Sui for metadata and governance, it delegates storage tasks to a set of separate nodes, thus avoiding the overhead of Sui validators.

At the core of Walrus is Red Stuff, a two-dimensional encoding protocol that enables efficient single-file encoding with robust data recovery capabilities. The system is secured through a staking-based WAL token incentive model, where nodes are rewarded for uptime and correct data handling and punished for failures or malicious behavior. The breakdown of the WAL tokenomics is as follows:

· Community Reserve: 43%

· Core Contributors: 30%

· Walrus User Airdrop: 10%

· Grants: 10%

· Investors: 7%

Technical Updates

Sui Core Development Project

Mysticeti V2 Update

Delphi Digital previously detailed Mysticeti v1 in the report "Sui Network: Unveiling the Mysterious Competitor." It eliminated the need for block validation by embedding submission rules directly into the DAG structure. This theoretically reduced the consensus latency of each block to as low as three message rounds, bringing Sui's consensus delay down from around 1900 milliseconds (Bullshark testnet) to about 390 milliseconds. Additionally, requiring only one signature per block reduced validator CPU load, increasing execution throughput and response speed.

The Mysticeti-FPC (v2) is an extension of Mysticeti-C (v1) that introduces a "Fast Path" for transactions that do not require full consensus, particularly useful for common scenarios such as token transfers or NFT minting, which only involve assets owned by a single address. Mysticeti-FPC does not operate as a standalone protocol (e.g., FastPay or Sui Lutris), but embeds the Fast Path logic into the same DAG, avoiding additional message passing, redundant cryptographic operations, and post-consensus checkpoints.

Move VM 2.0 Enhancements

Sui's Move VM v2 is a foundational optimization focused on execution efficiency and system composability. Core improvements include Arena Allocation, Package Caching, and Low Lock Contention, aimed at reducing latency under load. With cross-package pointer references (including system-level access), internal call speeds have seen significant improvement.

Additionally, this virtual machine has introduced a multi-stage abstract syntax tree (AST) for validation, optimization, and execution, as well as linking logic for cross-package virtual table resolution and updates to simplify modular development. Early benchmark tests have shown speedups ranging from 30% to 65% across various execution paths. This will enable Sui to expand into more complex, high-throughput use cases leveraging Move VM v2.

Execution Sharding with PilotFish

PilotFish is a horizontally scalable execution engine that overcomes the bottleneck of Sui's original single-machine execution model. Traditionally, Sui validators were monolithic, processing consensus, data retrieval, and state execution on a single machine, limited by vertical scaling constraints in compute, memory, and storage.

PilotFish decomposes this monolith into three distinct layers:

· Primary: Central coordinator handling transaction ordering and consensus;

· SequencingWorkers (SWs): Scalable nodes responsible for transaction extraction and routing;

· ExecutionWorkers (EWs): Horizontally distributed machines storing fragments of on-chain state and performing actual execution.

Pilotfish Sharding Workload Distribution:

· Each transaction is routed to a specific sequencer.

· Each on-chain object (i.e., state) is mapped to a specific executor.

Transactions needing access to objects across multiple shards are resolved through coordinated data exchange, which is a pull-based model where executors request remote state on demand. This maintains consistency without sacrificing parallel execution and closely integrates with Sui's lazy consensus design, which achieves consensus based on batched metadata rather than full transaction data.

This can achieve parallelism without shared memory, allowing computationally intensive workloads to linearly scale with available hardware. Benchmark testing shows that Pilotfish achieves up to a 10x throughput improvement using 8 EWs compared to a baseline execution engine.

Horizontal scaling paves the way for true resiliency in validator infrastructure. Unlike vertical scaling, which is constrained by hardware costs and configuration latency, horizontal scaling allows validators to elastically spin up commodity servers (such as 32-core servers on AWS or GCP) to meet demand spikes. If traffic persists, validators can migrate to more cost-effective bare-metal servers.

Its impact has three aspects:

· Validator operations become hardware-agnostic: no need for special high-end configurations;

· Infrastructure configuration becomes elastic and programmatic: automatically scales based on demand;

· Design space opens up new possibilities for Sui-native innovation, such as a package-specific fee market or priority queue, innovations achieved by Sui's object-centric state model.

This will make Sui one of the few environments capable of absorbing consumer-grade transaction throughput without increasing centralization or affecting latency.

Implementing an Object-Based Local Fee Market

Sui employs a multi-dimensional Gas pricing mechanism, dividing fees into two primary parts: computation fees and storage fees. So, how does Sui's local fee market operate in the Sui object environment?

Sui has implemented an Object-Based local fee market mechanism, which, unlike Ethereum, is more similar to Solana's fee structure. Sui sets fees based on specific requirements related to individual objects or assets. Each asset or application on Sui has an independent fee market, enabling local adjustments without impacting the entire network.

On the other hand, Ethereum operates a unified global fee market where each transaction contributes to overall network congestion, causing fees to rise across the chain during periods of increased demand. Similarly, Solana employs a localized fee market system, adjusting fees around specific contentious state objects or accounts.

Sui further extends this localization concept by directly associating fees with an "object" rather than "state." By linking fees to specific objects, Sui can process transactions involving different assets in parallel, avoiding fee interactions or congestion overflow. This isolation means that even if other applications on Sui are highly active, new applications can also achieve a high level of activity. For example, a popular trading pair on a DEX can independently adjust fees based on its own demand. As a result, Sui's object-level granularity in the localized fee market is more equitable for its user base and more efficient for its developer community.

Canonical Balance Accumulators

Sui's "Canonical Balance Accumulators" are designed based on objects, where balances are Move objects on the chain. These objects are not abstract concepts within contracts but independent, verifiable state objects. This setup achieves transaction-level parallelism as execution relies solely on access to specific objects rather than shared global storage.

Ethereum uses a centralized mapping in ERC-20 contracts to track balances. Each transfer triggers shared state, hindering parallelism and binding composability with contract-specific logic. Each token has its own implementation, often leading to integration edge cases.

On the other hand, Solana handles balances through token accounts, aiding in parallel execution. However, developers need to predefine all accounts for each transaction, creating resistance to building modular systems and limiting flexibility under dynamic conditions.

Sui simplifies this process. Standardized balance objects and managers like "BalanceManager" provide a clear way for the protocol to track and modify balances without holding state. Execution is horizontally scalable by default, with balance logic portable across modules without needing to wrap it in custom interfaces. Building and unlocking with object-level fee markets, isolation, and composability will be clearer without coordination overhead.

Multisignature Account Implementation

Sui's multisignature implementation is based on a weighted k-of-n signature model. Each signer is assigned a weight, and when the sum of all weights reaches or exceeds a preset threshold, the transaction is executed. This allows for flexible signature strategies, such as requiring 2 out of 3 signers or enforcing one key to always be signed together with other keys to achieve a setup similar to two-factor authentication (2FA).

The uniqueness of the Sui method lies in its support for using a heterogeneous key scheme within the same multisig. Users can mix Ed25519, secp256k1, and secp256r1 keys in a single authentication object, enabling more composable wallet and custody designs without the need for specialized tools.

Unlike threshold signatures that aggregate approvals into a single opaque signature, Sui's multisig exposes which keys signed which approvals. This enhances auditability and cross-party coordination without the need for complex multiparty computation (MPC) setups. Therefore, it is easier to reason about, easier to rotate participants, and natively compatible with the Sui transaction model.

MEV Developments on Sui

Priority Transaction Submission

At an execution level, Sui resolves conflicts on shared objects through a gas-based prioritization mechanism. Priority Gas Auctions (PGAs) serve as the primary coordination layer. As Sui's execution is object-centric and transactions modifying the same object must be serialized, PGAs act as a congestion pricing mechanism, particularly useful in object hotspots or DEX volatility.

SIP-19 introduced a soft bundling mechanism, submitting off-chain aggregated transaction groups as a unit. This enables reverse auctions (e.g., through Shio) where searchers can bid to have their transactions included in bundles with a high probability of execution.

SIP-45 introduced consensus amplification. Transactions with gas prices above kx RGP will be submitted multiple times by different validators, effectively amplifying their presence in consensus. This reduces fluctuations caused by validator asynchrony or leader rotations, ensuring the gas price accurately reflects inclusion priority, thereby curbing spam and improving fairness.

Mysticeti Block Streaming

One of the most intriguing upgrades Sui is undergoing is Block Streaming. Full nodes will be able to subscribe directly to consensus blocks, allowing access to pending transactions with a latency of less than 200 milliseconds before finality, reducing the on-chain searcher advantage and democratizing MEV opportunity capture.

Unlike off-chain relays, it is permissionless and open. It also provides a deterministic view of transaction ordering for third-party nodes, enabling speculative execution, arbitrage, and reentrancy logic to operate nearly in real-time.

Time-lock encryption is in the works to assist Sui in combating harmful MEV, and an MEV revenue distribution model is also being explored. Incentives will benefit validators, applications, and users, not just searchers.

DevX Update

Sui has seen some improvements in DevX. Move Registry has enhanced dependency management by introducing on-chain package naming and versioned imports, eliminating address-based fragile links. Key frameworks and libraries are being open-sourced with registry support, enabling developers to securely develop and upgrade applications. Additionally, Sui also features Programmable Transaction Blocks (PTB) replay and Move tracing capabilities to provide deep debugging support, allowing developers to step through transaction execution and precisely pinpoint fault states in multi-call processes.

Conclusion

Sui had several highlights in the last quarter. Both Mysticeti v2 and Pilotfish are not just regular upgrades; they will change how Sui handles transactions under load and how validators operate their infrastructure. Move VM 2.0 has also brought many improvements for developers building modular applications. These enhancements collectively propel Sui towards being able to truly support high-frequency use cases without adding coordination overhead.

In terms of the ecosystem, BTCfi is evidently becoming a wedge and may be favored by institutions. Protocols like Suilend and Aftermath are exploring new primitives that are natively compatible with the Sui architecture, such as object-based stablecoins, AMM lending pools, meta-tokens, and more. The interesting part now is observing how the fee market performs during demand spikes, whether MEV tools like soft bundling or block streaming will be adopted by searchers, and how infrastructure like Pilotfish will change validator economics in practice.

Additionally, Delphi Digital has observed an increase in institutional interest, with Canary Capital submitting an application for the Canary SUI ETF in the first quarter. Earlier reports indicated the involvement of financial institutions such as Grayscale, Franklin Templeton, VanEck, Libre, and Ant Group, all launching related investment products on the Sui network, ranging from tokenized funds to Exchange-Traded Notes (ETNs).

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.